Hello Julio,

I have a question about the Macaulay Duration formula you used to solve Excercise 1 in the Mock Exam.

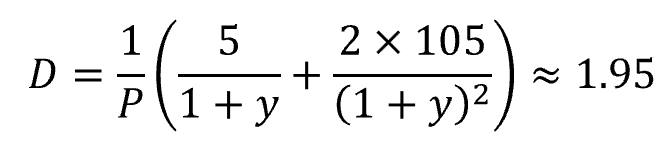

I understand that I also have to discount the Face Value and the last Coupon when I apply from the formula sheet, what you did above.

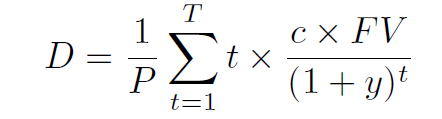

However, I am struggling to understand why you multiply the number of periods with the sum out of the Face Value and the last Coupon when the theoretical formula is:

If I apply thhis formula as follows, I have a slightly different solution. Is my Idea the wrong approach?

Thanks in advance for your help.