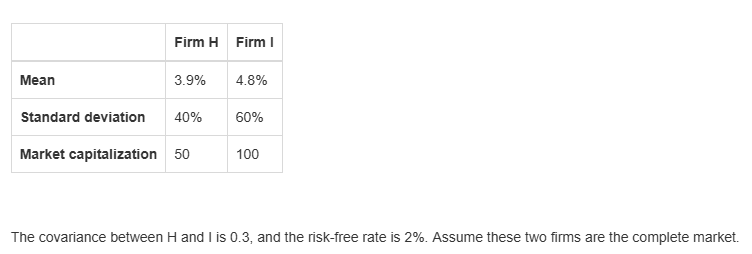

\(\beta_H = \dfrac{Cov(r_H,r_M)}{V(r_M)}\)

Let's start with the numerator:

\(Cov(r_H,r_M) = Cov(r_H, \frac{1}{3}r_H+\frac{2}{3}r_I) = \frac{1}{3}Var(r_H)+\frac{2}{3}Cov(r_H,r_I) = \frac{1}{3}0.4^2+\frac{2}{3}0.3 \approx 0.2533 \)

The denominator:

\(V(r_M) = \left(\frac{1}{3}\right)^2 V(r_H) + \left(\frac{2}{3}\right)^2 V(r_I) +2 \left(\frac{1}{3}\right) \left(\frac{2}{3}\right) Cov(r_H,r_I) \approx 0.3111 \)

Then

\(\beta_H \approx 0.8143\)

You can compute \(\beta_I\) in a similar way or use the market beta:

\(\frac{1}{3}\beta_H+\frac{2}{3}\beta_I=1\Rightarrow \beta_I = \frac{3}{2}-\frac{1}{2} \beta_H \approx 1.09\)